Ordinary and necessary job expenses which were not

reimbursed are deductible. Ordinary and

Tax Reporting

A taxpayer must report on his or her tax return if any of

the following apply.

• The

employee claims any job-related vehicle, travel, transportation, meal, or

entertainment expenses.

• The

employer reimbursed any reportable expenses.

• The

employee claims any job related expenses as a reservist, a qualified

performing artist, a fee-basis state or local government official, or an

individual with a disability claiming impairment-related work expenses.

Standard Mileage Rate

The business standard mileage rate for 2013 is 56.5¢ per

mile.

Examples of other job expenses deductible as unreimbursed employee expenses:

• Business

bad debt.

• Business

liability insurance premiums.

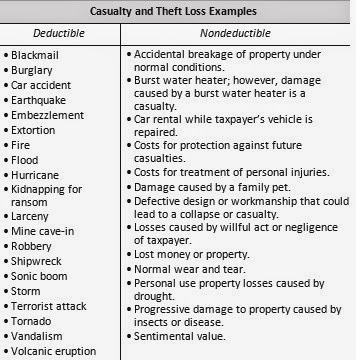

• Casualty

and theft losses of property used in performing services as an employee.

• Depreciation

on a computer or cell phone required by an employer.

• Dues to professional organizations and chambers of commerce if work related and

entertainment is not one of the main purposes of the organization. Any part of

dues that is for lobbying and political activities is nondeductible.

• Education

expenses related to work.

• Job

search fees to employment agencies and other costs to look for a new job in the

taxpayer’s present occupation, even if the taxpayer does not find a new job.

• Legal

fees related to work.

• Licenses

and regulatory fees.

• Lobbying

expenses to influence local legislation, and other exceptions to the general

rule.

• Malpractice

insurance premiums.

• Occupational

taxes.

• Office-in-home

expenses as an employee.

• Phone

charges for business use, but not the cost of basic service for the first phone

line into a residence.

• Physical

examinations required by employer.

• Protective

clothing required for work, such as hard hats, safety shoes, and glasses.

• Safety

equipment needed for work.

• Subscriptions

to professional journals and trade magazines related to work.

• Tools

and supplies used for work.

• Uniforms

required by employer that are not suitable for ordinary wear.

• Union

dues and expenses.

Job Search Expenses

Expenses incurred in looking for a new job in the taxpayer’s

present occupation are deductible, even if the taxpayer does not get a new job.

Job search expenses are not deductible for:

• Looking

for a job in a new occupation.

• A

substantial break between the ending of the last job and looking for a new job.

• The

taxpayer looking for a job for the first time.

Uniforms and Work Clothes

The cost and upkeep of uniforms and work clothes are

deductible if:

• The

taxpayer must wear them as a condition of employment, and

• The

clothes are not suitable for everyday wear.

• It

is not enough that the taxpayer wears unique or distinctive clothing on the

job, or that the taxpayer does not in fact wear the work clothing away from

work.

Lobbying Expenses

Expenses to influence legislation are not deductible.

Exceptions:

• Expenses

for attempting to influence the legislation of any local council or similar

local government, including an Indian tribal government.

•

Up to $2,000 per year (not counting overhead expenses)

for in-house expenses to influence legislation or communicating directly with a covered

executive branch official.

• Expenses of a professional lobbyist in the trade or business of lobbying on

behalf of another person.

Residential Telephone Line

The cost of local telephone service for the first telephone

line into a taxpayer’s residence is not deductible, even if it is used in a

trade or business. Any added charges for business use are deductible, such as

the cost of a second line, fax line, long distance, voice mail, internet

service, etc.

Unclaimed Reimbursements

If a taxpayer is entitled to be reimbursed by his or her

employer for job-related costs but does not put in a claim for reimbursement,

the costs are not deductible.

Travel Expenses

Travel expenses are ordinary and necessary expenses

incurred by a taxpayer while on temporary travel away from his or her tax home

for business purposes. A taxpayer travels away from his or her tax home if the

taxpayer’s business duties require an absence from home that is substantially

longer than a day’s work, and the taxpayer needs sleep or rest to meet the

demands of the work while away from home. The tax home includes the entire city

or general area in which the taxpayer’s business is located.

Standard meal

allowance. A taxpayer can substantiate meal and incidental expenses with a

standard meal allowance ($46 per day from October 1, 2012 through September 30,

2013). Additional amounts may apply for certain high-cost localities, based on

IRS Publication 1542, Per Diem Rates.

Lodging. Although an employer can

reimburse an employee tax free for qualified lodging at per diem rates, for an

employee or self-employed individual, only actual expenses are allowed for

lodging.